Q2 '23 Earnings Review

Highlighting some ideas from my coverage universe that beat estimates & raised guidance.

It is of course easier to explain something that has already happened than it is to predict the future but as investors, the best we can do is to update our worldview with the latest data and information and do our best to understand what this might mean for the story of the company. Earnings seasons are always eventful and I wanted to take some time to review some of the companies I have mentioned in past articles and some others that are within my coverage universe. I made a quick model for each to try to put the most recent numbers in context with the current share prices.

Airbnb (ABNB)

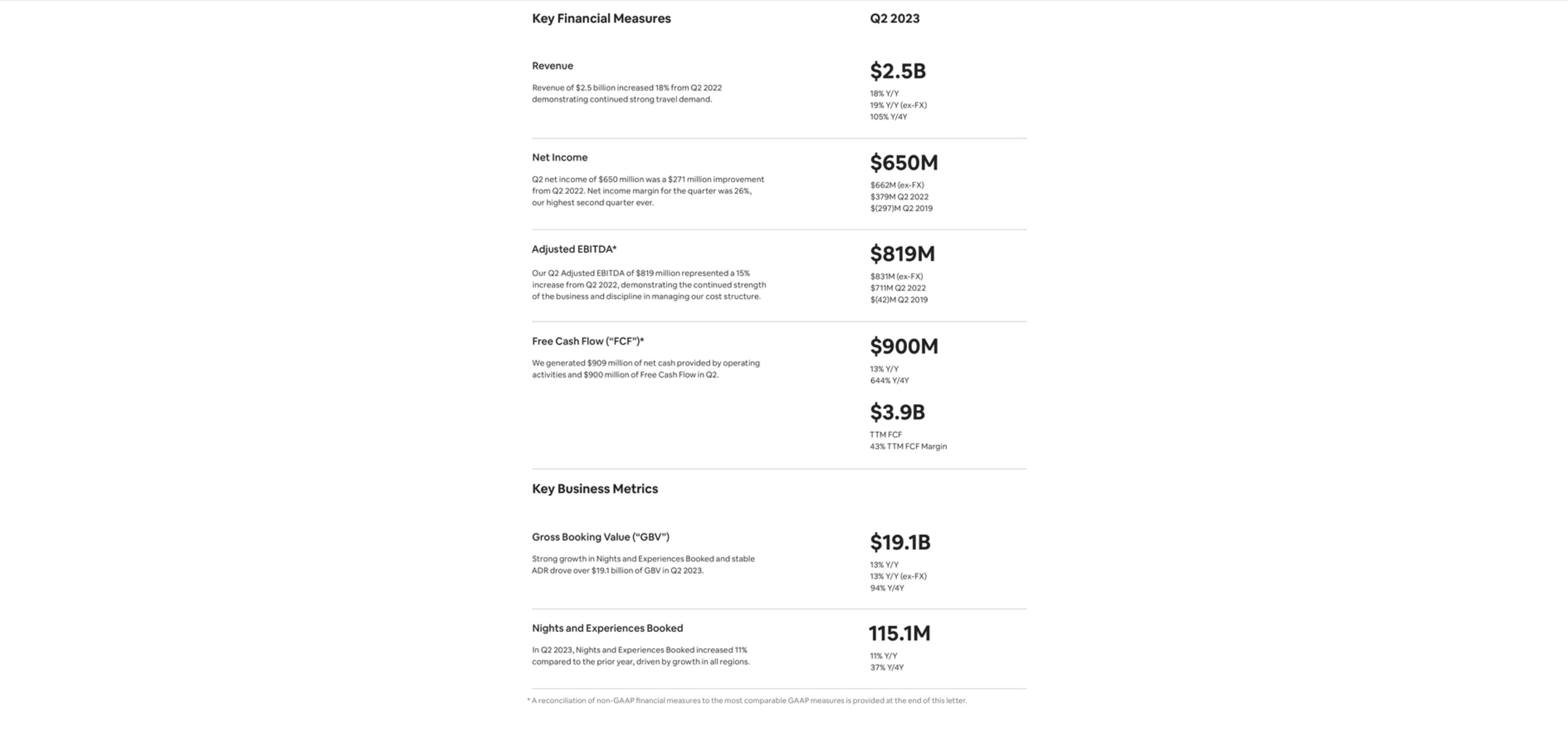

EPS $0.98 vs $0.80 EST

Revenue $2.5B vs $2.42B EST

Guidance of $3.3-$3.4B in revenue vs $3.22B EST

Airbnb had a solid quarter, beating estimate for earnings per share (EPS) and revenue, and raising guidance for next quarter, but shares were down after earnings as they only increased nights and experiences booked by 11% which were just under the consensus estimates for those metrics. Brian Chesky, the CEO, was optimistic about the company's performance and cited tough comparisons as to why the company missed the estimates for nights & experiences booked (a key metric that helps analysts understand the performance of the company.). The company announced new tools for hosts and Chesky mentioned the potential for Airbnb to explore an advertising platform as well as it’s efforts to leverage OpenAI’s ChatGPT to help make the customer service department more efficient. Airbnb’s strong performance comes in the wake of rumors about Airbnb rentals slowing (there was a tweet awhile back perpetuating the narrative that demand was slowing and prices were decreasing), online complaints about the many layers of fees that guests must pay (some of which were not previously included in the listed price of the rental, though this does seem to be something that management is aware of and is actively addressing) and worries about overall travel demand slowing down as consumers draw down their savings (the bear case would say that Airbnb is probably over-earning since travel is peaking and with student loan payments resuming, consumers are bound to spend less on travel.). This narrative seems to have made Airbnb a relatively popular short on the buyside, and while the numbers from last quarter are strong, the valuation is probably a little rich (the above model suggests the need for a 25% growth rate for the company’s pretax income in order to achieve a 8% IRR on the stock were you to buy it at $125.). However, the company is doing a lot of things well and has an incredibly strong cash position with about ~$10B of cash & short term investments on hand and another $9B in customer deposits. There is certainly substance to both sides of the story for Airbnb and I believe the company is worth following as they are a rare new era tech company who can generate fairly healthy free cash flow in what is still relatively early in the company’s lifetime (founded in 2008.)

Arista Networks (ANET)

EPS $1.58 vs $1.44 EST

Revenue $1.46B vs $1.38B

Guidance of $1.45-$1.5B in revenue vs $1.39 EST

Arista Networks (a company I did a write up on) posted a very strong quarter, driven by increased demand for AI networking. The company is strongly positioned for the AI arms race and the demand for their networking products is reflected in their record sales and profitability for the quarter. The company also raised guidance for next quarter and even with the 20% pop after their earnings report, the shares appear to be relatively fairly valued based on 16% projected earnings growth and 62% gross margins.

Axcelis Technologies (ACLS)

EPS $1.86 vs $1.46 EST

Revenue $274mm vs $257mm EST

Guidance of $280mm vs $261mm EST

Axcelis Technologies is a company that (per their website) delivers vital equipment, services and process expertise to the semiconductor manufacturing industry, helping customers reach higher levels of productivity with each new technology generation. Today, chipmakers from around the globe rely on their tools and technology insights to produce the transistors that power all electronics. Axcelis’ equipment portfolio comprises a powerful suite of manufacturing technologies for ion implantation - one of the most critical and enabling steps in the IC manufacturing process. They posted a very strong quarter, beating estimates for sales and EPS and raising guidance for next quarter as well. The CEO noted their is significant demand for their Purion Product family, especially in the silicon carbide market. They believe they are the only company with a product line that covers all implant recipes in mature technology markets. The company revised their revenue estimate for the full year to $1.1B, which is about a 20% year over year increase, and with 44% gross margins in the quarter (up from 41% in Q1) and the overall tailwinds for the entire semiconductor industry, one can certainly make the case that Axcelis is well positioned to capitalize on these trends. On a 5 year DCF, the shares appear to be a bit overvalued at their current level but overall business performance probably warrants putting Axcelis on your watchlist as it’s executing well in an industry (semiconductor capital equipment) that should continue to experience structural tailwinds from the increased demand for chips.

ELF Beauty (ELF)

EPS $0.93 vs $0.56 EST

Revenue $216.3mm vs $184.02mm EST

Guidance for next fiscal year revenue of $792-802mm vs $728.82mm EST

ELF Beauty (one of the companies mentioned in my Hyper Individualization write up) had a monster quarter, crushing estimates for both earnings and sales, and raising guidance for the next fiscal year as well. Earnings grew 182% year over year and sales were up 76.5% year over year. ELF has had a big run up this year, with shares up well over 100% already. It’s low cost cosmetic & skin care products are proving to be a hit with customers and the business is operating well - management cited a 260bps market share increase during the most recent quarter as well as a 280bps gross margin expansion which brings their gross margin to 71%. ELF CEO noted that they are one of only five publicly traded consumer companies out of 274 that has grown for 18 straight quarters and averaged at least 20% sales growth per quarter over that period. They believe they are still in the early innings of their long term growth story. Based on our model above, the shares appear to be overvalued by a fair bit, but this is often the case with high growth companies and DCFs aren’t necessarily the most effective way to model a company that is growing rapidly. We can expect ELF to keep investing in the business, both in e-commerce and physical retail channels and if earnings grow faster than our expectations, there may be an adequate return from current levels. Regardless, the company’s stellar performance merits consideration for a watchlist and if the overall market is to experience a pullback, the stock may reach levels that make it more attractive to a conservative investor.

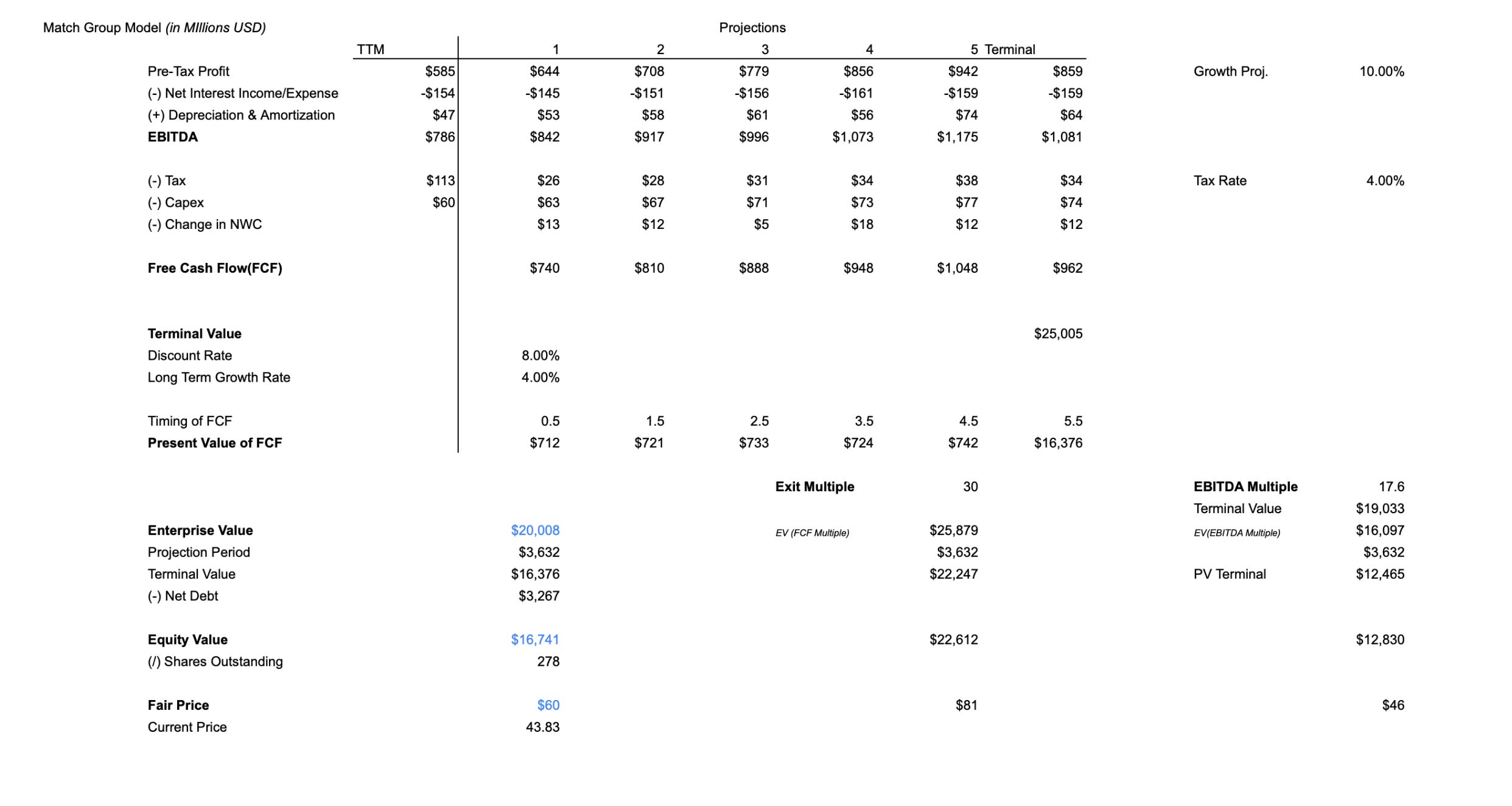

Match.com (MTCH)

EPS $0.48 vs $0.45 EST

Revenue $829.55mm vs $811.40mm EST

Guidance of $875-885mm in revenue vs $863.37mm EST

Match Group, the parent company of popular dating apps such as Hinge & Tinder (another company included in the Hyper Individualization write up), posted a strong quarter - beating estimates for earnings and sales and raising guidance for the next quarter as well. Though total payers declined slightly year over year, Tinder direct revenue was up 6% and Hinge direct revenue showed some acceleration, up 35% year over year. The company posted a solid 26% operating margin and highlighted the undergoing efforts to find more ways of monetizing their various online dating platforms. Management spoke about their commitment to delivering a refreshed user experience for Tinder and how they are focused on adapting the platform to meet the expectations of Gen-Z users, as well as how they are committed to innovation and integrating AI into their products over the long term. The above model suggests that if management is to be believed, and Match can deliver on it’s ambitious vision of growing it’s various dating platforms (and crucially, increasing the degree to which each is monetized) one could expect an 8% IRR if Match is indeed able to grow pretax profit at about ~10% per year. The company’s strong gross margin (~74%), increasing monetization of popular platforms and overall momentum across their portfolio of brands makes it an interesting company to watch and if they are able to capitalize on their expansion plans and effectively monetize their various platforms, may make the company an attractive long at current levels. The company’s efforts seem to be aligned with long term value creation for shareholders - revamping Tinder and increased focused on Gen-Z, expanding into Asia with the acquisition of Hyperconnect and further integrating AI into their platform, to name a few.

A few other companies that posted beat & raise quarters - Confluent (CFLT), KLA-Tencor (KLAC), Lam Research (LRCX), ServiceNow (NOW) & Uber Technologies (UBER). LVMH (LVMH) and Hermes (RMS) also posted solid quarters (companies that were included in the Hyper Individualization write up). I have models that I previously posted on Twitter X for KLA & Lam Research that I will post below and will write up my thoughts about the other companies (CFLT, NOW & UBER are harder to value with a DCF) in future posts. Thanks for reading, please reach out here or on Twitter X and let me know any thoughts and if you liked this post I will try to do more in the future!

KLA-Tencor Model (KLAC)

Lam Research Model (LCRX)

great job sophie

Helpful, thanks:)

P.S: Book review thread on X is excellent